Carl C. Icahn Issues Open Letter to

Shareholders of Southwest Gas

Sunny Isles Beach, Florida, October 20, 2021 — Today, Carl C. Icahn released the following open letter to the shareholders of Southwest Gas Holdings, Inc. (NYSE: SWX).

.

“John Hester lives in the right city – because he really seems to like playing roulette. What bothers us is that he is doing it with our money.” – Carl C. Icahn

.

______________________________________

.

.

.

Investor Contacts:

Harkins Kovler, LLC

Peter Harkins / Jordan Kovler

(212) 468-5390 / (212) 468-5384

[email protected] / [email protected]

.

.

.

CARL C. ICAHN

16690 Collins Avenue, Suite PH-1

Sunny Isles Beach, FL 33160

October 20, 2021

Fellow Shareholders:

This letter serves as a rebuttal to SWX management’s letter dated October 13, 2021. Management’s response to our letter exhibits two things:

- Management’s willingness to use shareholder money to pay bankers to help them obfuscate the truth.

- Management’s inability – even with bankers helping them – to make any good arguments.

WE BELIEVE SHAREHOLDERS ARE FED UP WITH MANAGEMENT’S GUISE AND WILL VOTE FOR OUR FULL SLATE OF DIRECTORS. THE VALUE DESTRUCTION MUST STOP. WE WELCOME ALL SHAREHOLDERS TO EITHER PARTICIPATE IN OUR ANY AND ALL TENDER OFFER AND RECEIVE $75 PER SHARE OR PARTICIPATE IN OUR PLAN FOR LONG-TERM VALUE CREATION TO BE EXECUTED BY OUR BLUE-RIBBON SLATE OF DIRECTORS.

Below are our responses to the statements made in SWX’s disingenuous and misleading letter, which we find insulting to the intelligence of all shareholders. But this is not surprising, given the authors – the SWX board and management team – barely qualify as shareholders. Collectively, they hold well under 1% of the company!

- SWX STATEMENT: Questar Pipelines Is an Especially Compelling Asset That Aligns with Southwest Gas Holdings

- ICAHN RESPONSE: We believe that SWX stockholders want to invest in a regulated utility; not a daily trip to the casino placing ratepayer money on lucky 7. Stockholders did not vest the officers and directors of SWX with the authority to run an unchecked investment company with a portfolio of unrelated assets, certainly not by diluting shareholders in order for management to further entrench themselves in their overpaid jobs while underperforming their competitors.

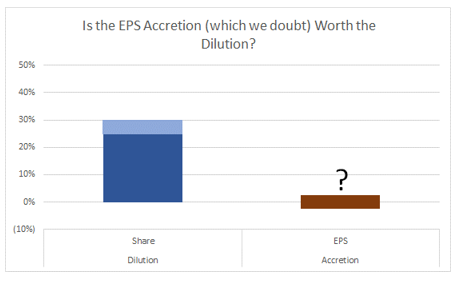

Management constantly states that the deal is accretive. How do we know? Management has provided no hard details – nothing by which to hold them accountable – with equity dilution still being one of the largest variables. Did management account for the significant stock decline following announcement? Even if the deal is accretive (which we doubt), is issuing >25% of the current market cap in equity and equity-linked securities worth a few pennies of EPS when there will very likely be an increased holding company discount? We are not alone in our accretion doubts. Bank of America recently wrote, “we see the deal as long-term dilutive given limited growth.”

**********

- SWX STATEMENT: The Acquisition of Questar Pipelines is Appropriately and Fairly Priced

- ICAHN RESPONSE: If an ordinary midstream company paid this price, we would say they overpaid, but have less to complain about. For a beleaguered company like SWX, however, with a stock that is massively undervalued in comparison to its peers, this deal is far from fair for the shareholders because of the dramatic equity dilution. The question remains: Why issue stock at 1x rate base to buy assets at 2x rate base, especially without synergies?

Other bidders were likely larger publicly traded midstream companies and private equity funds who have more ability to utilize leverage and less concerns about leverage impacting regulated utility subsidiaries. Also, management admitted there are minimal synergies, if any, and we believe there will actually be increased costs. Below is a quote from John Hester on a conference call after the deal announcement, and we found it amazingly uncompelling.

“We don’t really focus on synergies. We think there may be some of those available. As Karen was mentioning earlier, we’ve got a transition services agreement in place with Dominion of some of the services that were provided to the Questar Pipelines asset, were provided by Dominion. So when that transition services agreement ends, we will have to — or, rather along that path, we will be adding some employees.”

**********

- SWX STATEMENT: Our Financing Plan Rebalances Our Capital Structure and Supports Our Balance Sheet

- ICAHN RESPONSE: If SWX really wanted to improve its balance sheet, it would cancel this absurd acquisition, sell Centuri, and use a portion of the proceeds to improve the balance sheet, allocating some portion of the proceeds towards the funding of future growth. Contrary to that, adding HoldCo debt as planned reduces financial flexibility.

**********

- SWX STATEMENT: Assertions in Your October 4th Letter Negatively Comparing Our Earned ROE to Other Utilities Are Inaccurate

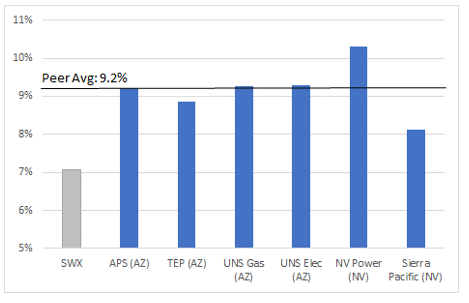

- ICAHN RESPONSE: There is nothing subjective or unreasonable in our numbers. We use the ROE excluding the extra COLI income, and we strictly present all the relevant comps in Nevada and Arizona. They ALL delivered much higher ROEs. Furthermore, each of these comps is exposed to strong customer growth. UNS Gas (though small) is 100% gas in Arizona and averaged a 10.3% ROE over the past four years. Management consistently blames the ROE underperformance on regulatory lag. We believe that all of the below companies suffer from regulatory lag but only SWX dramatically underperforms.

**********

- SWX STATEMENT: We Have a Long and Demonstrated History of Constructive Relationships with Our Regulators

- ICAHN RESPONSE: Did you read the filings from last two general rate cases in Nevada? In case you forgot, the Review Journal published two articles titled, “SOUTHWEST GAS WANTS TO RAISE NEVADA RATES TO PAY FOR HOMES, MASSAGES” and “FANCY DINNERS, CAR RIDES FOUND IN SOUTHWEST GAS RATE REQUEST.”

**********

- SWX STATEMENT: Our Shareholder Returns Continue to Climb

- ICAHN RESPONSE: Focusing on share price performance since February 2020 is nonsensical. 30% of SWX’s business is the services division and that division’s peers have tripled, so adjusting for that clearly implies that SWX’s core LDC operations have meaningfully underperformed comps. A stock price chart that starts in February 2020 also misses the 20% underperformance in 2019. If you want to pick a short time period to examine, we suggest more recent history. The stock fell when the deal was leaked. The stock increased when we announced our opposition. The stock fell when the deal was formally announced.

**********

- SWX STATEMENT: We Remain Disciplined On G&A Costs as Part of Our Overall O&M Costs

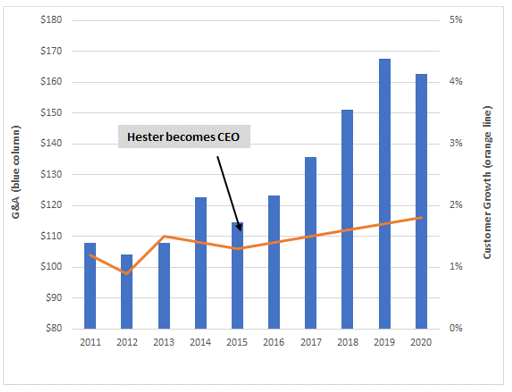

- ICAHN RESPONSE: We are not sure how a 42% increase in G&A is disciplined. It is likely no coincidence that in 2015, the year that John Hester became CEO, G&A started astronomically increasing. Prior to Hester, SWX managed to keep G&A essentially flat despite having similar growth trends during the whole period. Wonder what changed? All signs point to Hester’s mismanagement. How did G&A go up so much? And even if SWX can manage to lower other operating costs shouldn’t those $ accrue to ratepayers through lower bills rather than pad management wallets?

**********

- SWX STATEMENT: This Transaction Increases Strategic Optionality and Flexibility

- ICAHN RESPONSE: Management is keen on using words like “optionality” to discuss Centuri. They will dangle the “optionality” carrot to analysts and shareholders, buying months and quarters and years. Don’t be fooled. See below comment from the 2018 Analyst Day. Sound familiar?

Shareholder: “Any update on the thinking to perhaps separating Centuri from Southwest in any way?”

CEO: “As the business continues to grow, we believe that, that does tend to incrementally increase what we could call its optionality is the possibility of having a publicly traded equity like you say – like you suggest, a possibility some time down the road. I would say, certainly that is a possibility”

**********

- SWX STATEMENT: Board Oversight Is Strong and Average Tenure Has Decreased

- ICAHN RESPONSE: SWX sounded proud to state a tenure of 10.8 years on average. That does not seem worthy of praise. Excluding the most recent two additions (the only 2 individuals with any utility experience) the tenure of the other directs was almost 14 years. With respect to whether or not oversight is strong, tenure is one issue, but ownership is another. As we noted earlier of the last proxy update, management and the Board of Directors combined owned less than 1% of this company. Where is the oversight and accountability when a CEO receives a major compensation increase to over $6.5 million per year for doing a terrible job? How has the board overlooked the fact that G&A has gone up 42% during Hester’s tenure?

**********

- SWX STATEMENT: Our Executive Compensation Is Well-Aligned to Support Long-Term Shareholder Value

- ICAHN RESPONSE: It is unclear to us why compensation increased 25% in 2019 and 27% in 2020 while the company underperformed the S&P utilities index by 24% and 18%, respectively, in those years. We look forward to seeing next year’s say on pay results.

**********

For all these reasons, we believe our proxy contest and tender offer are in the interest of all stakeholders (except for senior management and the Board of Directors). We urge shareholders to speak to management and the Board and let them know how they feel about management’s recent actions. We urge shareholders to vote for our upcoming slate and decide whether to tender their shares or participate in long-term value creation.

.

.

.

Additional Information and Where to Find It;

Participants in the Solicitation and Notice to Investors

SECURITY HOLDERS ARE ADVISED TO READ THE PROXY STATEMENT AND OTHER DOCUMENTS RELATED TO THE SOLICITATION OF PROXIES BY CARL C. ICAHN AND HIS AFFILIATES FROM THE STOCKHOLDERS OF SOUTHWEST GAS HOLDINGS, INC (“SOUTHWEST GAS”). USE AT THE ANNUAL MEETING OF STOCKHOLDERS OF SOUTHWEST GAS WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION, INCLUDING INFORMATION RELATING TO THE PARTICIPANTS IN SUCH PROXY SOLICITATION. WHEN COMPLETED, A DEFINITIVE PROXY STATEMENT AND A FORM OF PROXY WILL BE MAILED TO STOCKHOLDERS OF SOUTHWEST GAS AND WILL ALSO BE AVAILABLE AT NO CHARGE AT THE SECURITIES AND EXCHANGE COMMISSION’S (“SEC”) WEBSITE AT HTTP://WWW.SEC.GOV. INFORMATION RELATING TO THE PARTICIPANTS IN SUCH PROXY SOLICITATION IS CONTAINED IN THE SCHEDULE 14A FILED BY CARL C. ICAHN AND HIS AFFILIATES WITH THE SECURITES AND EXCHANGE COMMISSION ON OCTOBER 5, 2021. EXCEPT AS OTHERWISE DISCLOSED IN THE SCHEDULE 14A, THE PARTICIPANTS HAVE NO INTEREST IN SOUTHWEST GAS.

THE SOLICITATION DISCUSSED HEREIN RELATES TO THE SOLICITATION OF PROXIES FOR USE AT THE 2022 ANNUAL MEETING OF STOCKHOLDERS OF SOUTHWEST GAS HOLDINGS.

THE PROPOSED TENDER OFFER MENTIONED ABOVE HAS NOT YET COMMENCED. THIS COMMUNICATION IS FOR INFORMATIONAL PURPOSES ONLY AND IS NOT A RECOMMENDATION, AN OFFER TO PURCHASE OR A SOLICITATION OF AN OFFER TO SELL SHARES. AT THE TIME THE TENDER OFFER IS COMMENCED, AFFILIATES OF ICAHN ENTERPRISES WILL FILE A TENDER OFFER STATEMENT AND RELATED EXHIBITS WITH THE SEC AND SWX WILL FILE A SOLICITATION/ RECOMMENDATION STATEMENT WITH RESPECT TO THE TENDER OFFER WITH THE SEC. STOCKHOLDERS OF SWX ARE STRONGLY ADVISED TO READ THE TENDER OFFER STATEMENT (INCLUDING THE RELATED EXHIBITS) AND THE SOLICITATION/RECOMMENDATION STATEMENT, AS THEY MAY BE AMENDED FROM TIME TO TIME, WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION THAT STOCKHOLDERS SHOULD CONSIDER BEFORE MAKING ANY DECISION REGARDING TENDERING THEIR SHARES. IF THE TENDER OFFER IS COMMENCED, THE TENDER OFFER STATEMENT (INCLUDING THE RELATED EXHIBITS) AND THE SOLICITATION/RECOMMENDATION STATEMENT WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT WWW.SEC.GOV. IN ADDITION, IF THE TENDER OFFER IS COMMENCED, THE TENDER OFFER STATEMENT AND OTHER DOCUMENTS THAT ARE FILED BY ICAHN ENTERPRISES (OR ITS AFFILIATES) WITH THE SEC WILL BE MADE AVAILABLE TO ALL STOCKHOLDERS OF SWX FREE OF CHARGE UPON REQUEST TO THE INFORMATION AGENT FOR THE TENDER OFFER. THE INFORMATION AGENT FOR THE TENDER OFFER WILL BE HARKINS KOVLER, LLC, 3 COLUMBUS CIRCLE, 15TH FLOOR, NEW YORK, NY 10019, TOLL-FREE TELEPHONE: +1 (800) 326-5997, EMAIL: [email protected].

Other Important Disclosure Information

SPECIAL NOTE REGARDING THIS LETTER:

THIS LETTER CONTAINS OUR CURRENT VIEWS ON THE VALUE OF SOUTHWEST GAS SECURITIES AND CERTAIN ACTIONS THAT SOUTHWEST GAS’ BOARD MAY TAKE TO ENHANCE THE VALUE OF ITS SECURITIES. OUR VIEWS ARE BASED ON OUR OWN ANALYSIS OF PUBLICLY AVAILABLE INFORMATION AND ASSUMPTIONS WE BELIEVE TO BE REASONABLE. THERE CAN BE NO ASSURANCE THAT THE INFORMATION WE CONSIDERED AND ANALYZED IS ACCURATE OR COMPLETE. SIMILARLY, THERE CAN BE NO ASSURANCE THAT OUR ASSUMPTIONS ARE CORRECT. SOUTHWEST GAS’ PERFORMANCE AND RESULTS MAY DIFFER MATERIALLY FROM OUR ASSUMPTIONS AND ANALYSIS.

WE HAVE NOT SOUGHT, NOR HAVE WE RECEIVED, PERMISSION FROM ANY THIRD-PARTY TO INCLUDE THEIR INFORMATION IN THIS LETTER. ANY SUCH INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN.

THIS LETTER ALSO REFERENCES THE SIZE OF OUR RESPECTIVE CURRENT HOLDINGS OF SOUTHWEST GAS SECURITIES. OUR VIEWS AND OUR HOLDINGS COULD CHANGE AT ANY TIME. WE MAY SELL ANY OR ALL OF OUR HOLDINGS OR INCREASE OUR HOLDINGS BY PURCHASING ADDITIONAL SECURITIES. WE MAY TAKE ANY OF THESE OR OTHER ACTIONS REGARDING SOUTHWEST GAS WITHOUT UPDATING THIS LETTER OR PROVIDING ANY NOTICE WHATSOEVER OF ANY SUCH CHANGES (EXCEPT AS OTHERWISE REQUIRED BY LAW).

FORWARD-LOOKING STATEMENTS:

Certain statements contained in this letter are forward-looking statements including, but not limited to, statements that are predications of or indicate future events, trends, plans or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties. Forward-looking statements are not guarantees of future performance or activities and are subject to many risks and uncertainties. Due to such risks and uncertainties, actual events or results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Forward-looking statements can be identified by the use of the future tense or other forward-looking words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “should,” “may,” “will,” “objective,” “projection,” “forecast,” “management believes,” “continue,” “strategy,” “position” or the negative of those terms or other variations of them or by comparable terminology.

Important factors that could cause actual results to differ materially from the expectations set forth in this letter include, among other things, the factors identified in Southwest Gas’ public filings. Such forward-looking statements should therefore be construed in light of such factors, and we are under no obligation, and expressly disclaim any intention or obligation, to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

.

.