FOR IMMEDIATE RELEASE

Contact:

Icahn Capital LP

Susan Gordon

(212) 702-4309

CARL ICAHN ISSUES OPEN LETTER TO

TIM COOK, CHIEF EXECUTIVE OFFICER OF APPLE

New York, New York, May 18, 2015 – Today Carl Icahn released the attached open letter to Tim Cook, the Chief Executive Officer of Apple Inc.

For more information on this and other topics, follow Carl Icahn on Twitter at:

@Carl_C_Icahn

https://twitter.com/Carl_C_Icahn

ALL RECIPIENTS ARE ADVISED TO READ

“IMPORTANT DISCLOSURE INFORMATION”

AT THE END OF THE ATTACHED LETTER

Carl C. Icahn

767 Fifth Avenue, 47th Floor

New York, New York 10153

May 18, 2015

Dear Tim:

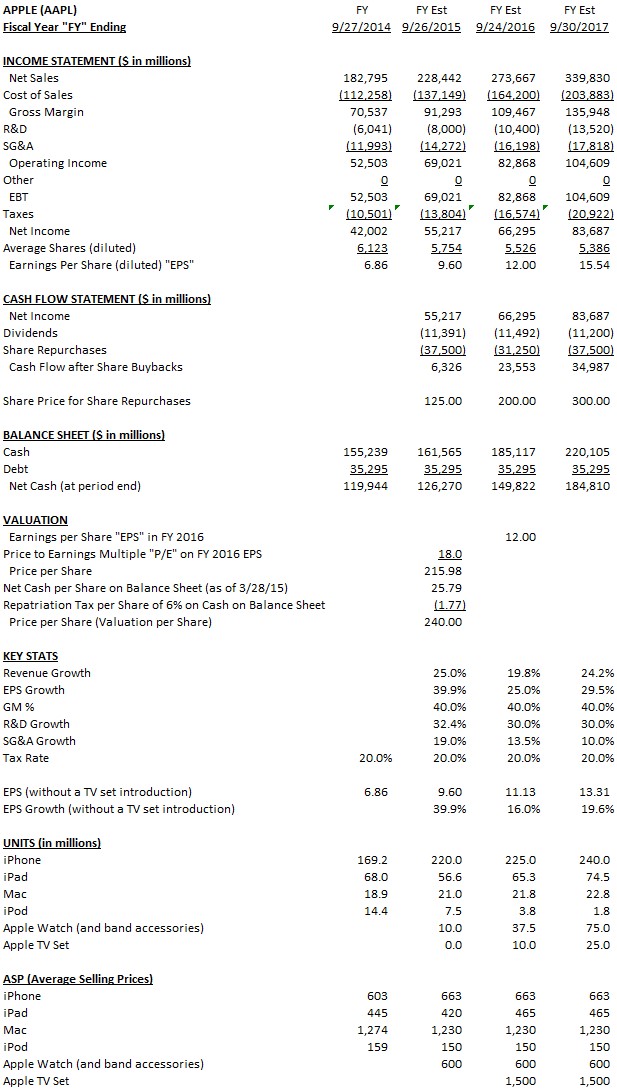

We again applaud you and the rest of management for Apple’s impressive operational performance and growth. It is truly impressive that, despite severe foreign exchange headwinds and massive growth in investment (in both R&D and SG&A), the company will still grow earnings by 40% this year, according to our forecast. After reflecting upon Apple’s tremendous success, we now believe Apple shares are worth $240 today. Apple is poised to enter and in our view dominate two new categories (the television next year and the automobile by 2020) with a combined addressable market of $2.2 trillion, a view investors don’t appear to factor into their valuation at all. We believe this may lead to a de facto short squeeze, as underweight actively managed mutual funds and hedge funds correct their misguided positions. To arrive at the value of $240 per share, we forecast FY2016 EPS of $12.00 (excluding net interest income), apply a P/E multiple of 18x, and then add $24.44 of net cash per share. Considering our forecast for 30% EPS growth in FY 2017 and our belief Apple will soon enter two new markets (Television and the Automobile) with a combined addressable market size of $2.2 trillion, we think a multiple of 18x is a very conservative premium to that of the overall market. Considering the massive scope of its growth opportunities and track record of dominating new categories, we actually think 18x will ultimately prove to be too conservative, especially since we view the market in general as having much lower growth prospects.

We are pleased that Apple has directionally followed our advice and repurchased $80 billion of its shares (yielding the company’s shareholders an excellent return), but the company’s enormous net cash position continues to grow while the company’s shares are still dramatically undervalued. With Apple’s shares trading for just $128.77 per share versus our valuation of $240 per share, now is the time for a much larger buyback. We appreciate that the Board just increased the share repurchase authorization by $50 billion, and that it continues to prioritize share repurchases over dividends (as it should). We again simply ask you to help us convince the board of how these two underlying issues (inefficient net cash growth and share undervaluation) persist and combine to enhance the opportunity for accelerated share repurchases in greater magnitude. We also ask you to help us convince the board that this is not a choice between investing in growth and share repurchases. As our model forecasts, despite more than 30% growth in R&D annually through FY 2017 to $13.5 billion (up from $1.8 billion in FY 2010) and your updated capital return program, Apple’s net cash position (currently the largest of any company in history) will continue to build on the balance sheet.

It is our belief that large institutional investors, Wall Street analysts and the news media alike continue to misunderstand Apple and generally fail to value Apple’s net cash separately from its business, fail to adjust earnings to reflect Apple’s real cash tax rate, fail to recognize the growth prospects of Apple entering new categories, and fail to recognize that Apple will maintain pricing and margins, despite significant evidence to the contrary. Collectively, these failures have caused Apple’s earnings multiple to stay irrationally discounted, in our view.

When we compare Apple’s P/E ratio to that of the S&P 500 index, we find that the market continues to value Apple at a significantly discounted multiple of only 10.9x, compared to 17.4x for the S&P 500, awarding the S&P500 with a 60% premium valuation to Apple:

Importantly, as we have noted previously, we assume a 20% tax rate for the purpose of forecasting Apple’s real cash earnings, not the 26.2% “effective” tax rate used by Apple, and view this as a necessary adjustment, often overlooked by both analysts and investors. For more detail on our methodology for this adjustment, please review our letter titled “Carl Icahn Issues Letter to Twitter Followers Regarding Apple” published February 11th, 2015, which you can find here: https://carlicahn.com/letter-to-twitter-followers-regarding-apple/

By applying this adjustment to the current consensus FY2015 EPS of $8.96 (among the 45 analysts who have updated their EPS targets since April 22nd), the adjusted result is $9.71. Notably, while previously criticized by some of these analysts as being too aggressive, this consensus EPS forecast, which includes interest income, is now largely in line with our own forecast of $9.60, which does not include interest income. And, once again, we exclude interest income from our EPS forecast because we value Apple’s enormous net cash balance separately from the enterprise, unlike most analysts.

While our forecast for FY 2016 EPS is significantly above Wall Street consensus today, in October 2014 so was our original forecast for FY 2015 EPS, which is now in line with the Wall Street consensus. We are optimistic that ecosystem improvements (Apple Watch, Apple Pay, Homekit and Healthkit in particular) will drive modest growth in iPhone revenues next year, despite the difficult comparison that will result from iPhone’s tremendous performance this year. With a new iPhone expected in September 2016, Apple stands to benefit as iPhone continues to take premium market share (switchers from competitors), as the middle class continues to grow in emerging markets, and as the modest level of upgrades (only 20% to date) indicates pulling demand forward from FY 2016 to FY 2015 may not be as severe as some have highlighted. Along with a more dramatic push into the TV market, increasing traction with Apple Watch, and the introduction of a larger screen iPad, we have confidence in our forecast for FY 2016.

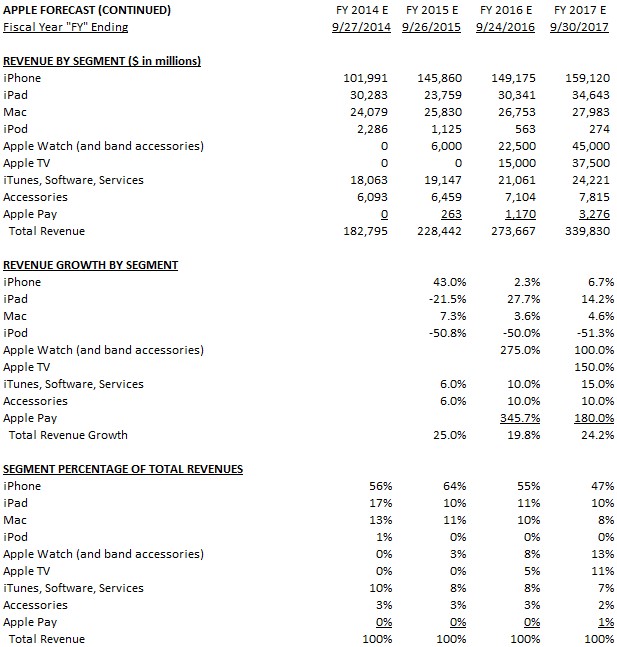

We believe Apple Watch, Apple Pay, Homekit, Healthkit, Beats Music, and further innovation in existing product lines collectively represent a tremendous opportunity that on their own justify a valuation that, at the very least, reflects a market multiple. That being said, we share your excitement that “our best days are ahead of us” and that Apple has “no shortage of growth opportunities to pursue.” The company’s dramatic increase in R&D spending should signal to investors that Apple plans to aggressively pursue these growth opportunities. It may be difficult for some to fathom (only because Apple is already the largest company in the world), but Apple is very much a long term growth story from our perspective, which is exactly why we believe the company’s shares should trade at a premium multiple to the S&P 500, as opposed to the S&P 500 trading at a 60% premium to Apple. While we respect and admire Apple’s predilection for secrecy, the company’s aggressive increases in R&D spending (and some of the more well-supported rumors) have bolstered our confidence that Apple will enter two new product categories: television and cars. Combined, these two new markets represent $2.2 trillion, three times the size of Apple’s existing markets (if we exclude Apple Watch).

Excluding advertising, the addressable market for television is approximately $575 billion, which is larger than the smartphone market. Also, given that people spend an average of 12% of the day watching TV (equating to 25% of their free time), we view television’s role in the living room as a strategically compelling bolt-on to the Apple ecosystem. In addition to an Ultra High Definition television set, we expect Apple to launch a related suite of tiered products and services, including a “skinny bundle” of pay-tv channels (partnered with various media companies) and an updated Apple TV microconsole (which will continue to service the massive install base of televisions offered by other OEMs). This will enable Apple to pursue the entire market by offering multiple products at various price points across the demographic spectrum. Netflix offers a similar tiered approach to pricing today by charging a higher price for those seeking the ability to receive ultra high definition content.

We believe this move into TV will also benefit all the other devices and services in the Apple ecosystem. As just one of many possible examples of this, the Apple Watch could perhaps be used as a remote control. Similarly, as we expect Apple to launch a larger 12.9” iPad, it would offer an enhanced viewing experience for an Apple pay tv service, or act an improved “second screen” to an Apple UltraHD television.

At $1.6 trillion, the enormous addressable market for new cars is approximately four times the size of the smartphone market. It’s estimated that people spend an average of 1 hour every day traveling, mostly in cars, but not everyone drives, implying that the average time that daily commuters spend in a car is much higher. We believe the rumors that Apple will introduce an Apple-branded car by 2020, and we believe it is no coincidence that many believe visibility on autonomous driving will gain material traction by then.

As autonomous driving would release drivers’ attention from the activity of driving and navigating, and perhaps even increase the time people actually want to spend inside a car, both an automobile and the services provided therein become even more strategically compelling. While Apple currently addresses this market with CarPlay, it seems logical that Apple would view the car itself as a the ultimate mobile device to which it could bring its peerless track record of marrying superior industrial design with software and services, along with its globally admired brand, and offer consumers an overall automobile experience that not only changes the world but also adds a robust vertical to the Apple ecosystem. And for Apple, the car market is more than big enough to “move the needle” significantly, even as the world’s largest company.

The rising cost of oil, its impact on global warming, the geopolitical risks associated with oil dependency (especially as fuel for automobiles), followed more recently by the rise of cost effective alternatives presents a “change the world” opportunity for Apple. It is widely believed that the electric battery will play a key role in this transition. The lithium-ion battery already represents a critical component across many of Apple’s existing products (iPhone, iPad, Apple Watch, MacBook, Beats) and any further innovation could be a “game changer” in terms of both battery life and form factor across Apple’s entire ecosystem. Since lithium-ion batteries represent a large percentage of the cost of today’s electric vehicle, we believe Apple should be well positioned to leverage its existing knowledge domain and more robust R&D spending in this area, and in turn apply any energy density / battery life improvements for a car across all the other products in its ecosystem that will share the benefit from such battery innovation (iPhone, iPad, Apple Watch, MacBook, Beats).

As a mobile device that is differentiated by design, brand, and consumer experience where software and services are increasingly critical, an Apple car would seem to be uniquely positioned.

While the television and the car offer tremendous growth opportunities, Apple’s core ecosystem continues to improve and grow, now sometimes referred to as a “mega-ecosystem”, a term we find increasingly appropriate, as we look at the breadth of its components, which now include existing products (iPhone, Apple Watch, Mac, iPad, Beats, Apple TV), software/services (Apple Pay, Homekit, Healthkit, Carplay, iCloud, iTunes, and rumored Beats Music, pay TV service), as well as possible new products in new categories (a Car, a TV set). Furthermore, ongoing innovations and enhancements to all of the above will drive even more premium market share gains for iPhone, which sits at the epicenter of this mega-ecosystem.

Apple has clearly demonstrated a track record of excellence and success when entering new categories. We expect this to continue with the Apple Watch, the television, and the car, and the world will look back on today’s undervaluation as a fascinating example of market inefficiency (and likewise on our valuation at 18x earnings per share as conservative). Because of this, we encourage both accelerated and larger-magnitude share repurchases as you consider how to allocate capital going forward. As you continue to evaluate this opportunity, and consider the right prices at which to opportunistically repurchase shares, we hope you give credence to our advice in light of our investment record. Unlike the many actively managed mutual funds and hedge funds that are underweight Apple and have underperformed the S&P 500, we have exhibited strong outperformance, thanks in part to our large position in Apple. The Sargon Portfolio (a designated portfolio of assets co-managed by Brett Icahn and David Schechter within the private investment funds comprising Icahn Enterprises’ Investment segment and High River Limited Partnership, subject to the supervision and control of Carl Icahn) has generated annualized gross returns of 36.9% since its formation on April 1, 2010 through April 30, 2015 with $8 billion of assets under management as of April 30, 2015.

If you choose not to pursue some of the new categories we highlighted, or you find our growth forecasts too aggressive for any one new category in particular, we’ll be the first to admit that you are more knowledgeable in these areas than we are. But we believe, that under any circumstances, you would agree that in the aggregate, all these new categories taken together (along with those of which we may be unaware) represent one of the greatest growth stories in corporate history, as well as one of the greatest opportunities ever for a company to invest in itself by repurchasing its shares.

Sincerely,

Carl C. Icahn

Brett Icahn

David Schechter

Key Assumptions

- iPhone – after our estimate of 43% revenue growth in FY 2015, we forecast modest revenue growth in FY 2016 of just 2.3%, followed by moderate revenue growth of 6.7% in FY 2017, all driven by volume growth amidst flat average selling prices over the three year period paced by switchers, new middle class users, ecosystem strength, and innovation

- iPad – after disappointing revenue growth of negative 21.5% in FY 2015 as cannibalization from the larger screen iPhone and customers utilizing existing older models for longer than we expected impacted results, we forecast Apple is at an inflection point and expect the introduction of a new larger screen iPad in conjunction with its push into television, penetration into the enterprise, maturation of the replacement cycle, new middle class users, ecosystem strength, and innovation to drive strong performance with revenue growth of 27.7% in FY 2016 and 14.2% in FY 2017.

- Mac – in a declining PC industry, we expect Mac to continue its market share gain and support our forecast for its strong performance of 7.3% revenue growth in FY 2015, followed by 3.6% in FY 2016, and 4.6% in FY 2017 on flat average selling prices over the three year period of $1,230.

- Apple Watch – after the recent release in the 2nd half of FY 2015, we expect the Apple Watch to gain traction and be a success in the market leading our forecasts of 10 million units during the 2nd half of FY 2015 at $600 average selling prices including the extra bands many consumers will order. Throughout FY 2016 we expect the Apple Watch to gain further traction and a second generation Apple Watch to be released sometime in 2nd half of FY 2016. We expect improvements in both the number and quality of Apps along with adding sensors and functionality in later generations of the Apple Watch to evolve the Apple Watch into a must have accessory over time for iPhone owners. We forecast revenues of $6 billion in FY 2015, $22.5 billion in FY 2016, and $45 billion in FY 2017.

- Apple Television Set – after many years of rumors as part of Apple’s push into television and as we referenced previously, we expect in FY 2016 Apple will sell 55” and 65” ultra high definition television sets. We forecast revenues of $15 billion in FY 2016 and $37.5 billion in FY 2017 on 10 million and 25 million units respectively with average selling prices of $1,500.

- iTunes, Software, & Services – as part of Apple’s move into television, we expect the introduction of a “skinny bundle” of pay-tv channels (partnered with various media companies) and video content sold through iTunes, along with a Beats Music subscription service and App Store sales give us comfort in our forecasts of growth over the next three years of 6% in FY 2015, 10% in FY 2016, and 15% in FY 2017. Not to mention HomeKit and HealthKit which for now we expect to not be monetized but simply enhance the overall ecosystem.

- Accessories and iPod – as part of Apple’s move into television, we expect the introduction of an updated Apple TV microconsole (which will continue to service the massive install base of televisions offered by other OEMs), along with improvements to Beats headphones to drive growth far in excess of the decline in iPod which at our forecast $1.1 billion of revenues in FY2015 is largely irrelevant to Apple financially

- Apple Pay – after an insignificant financial contribution in FY 2015 we expect Apple Pay to gain acceptance at more retailers and for Apple to expand the service internationally. Our forecasts for revenues (also equivalent to gross margins as the variable costs are de minimis) are $263 million in FY 2015, $1.2 billion in FY 2016, and $3.3 billion in FY 2017.

- Gross Margins – we forecast flat gross margins of 40.0% from FY 2015 through FY 2017.

- Research and Development “R&D” – we forecast robust growth in R&D as Apple ramps its investments in innovation at a breathtaking pace with growth of 32.4% , 30% , and 30% over the next three years to $13.5 billion in FY 2017 (up from $1.8 billion spent in FY 2010).

- Selling, General, & Administrative “SG&A” – we forecast heavy investment in SG&A, as it rises by 19%, 13.5%, and 10% over the next three fiscal years to $17.8 billion in FY 2017.

- Interest Income – with regards to interest income, since we value the net cash separately from the business, we assume no interest income from Apple’s net cash of $149.7 billion on March 28, 2015.

- Effective Tax Rate – importantly for the company’s income tax rate, we consider 20% a more appropriate tax rate for the purposes of forecasting real earnings, not the 26% effective tax rate Apple uses in their income statement. Most companies in the S&P 500 state that they plan to permanently reinvest their international earnings and therefore do not have to accrue for an income tax on unremitted earnings and thus show a lower tax rate. Google is a good example of this, as its effective tax rate is 20%. Apple, unlike Google and most companies in the S&P 500 has chosen to accrue income taxes on some of its unremitted international earnings and according has an effective tax rate of 26%. Therefore, when assessing the multiple of earnings at which Apple should trade, we believe it is appropriate to use a 20% tax rate for Apple in order to make such comparisons Apples to Apples, no pun intended.

- Share Repurchases – we assume share repurchases of $37.5 billion, $31.25 billion, and $37.5 billion over the next three year for our forecast and not the more aggressive pace we hope the Board will undertake

- Cash Flow – for simplicity purposes, we assume net income equals cash flow other than dividends and share repurchases

- Valuation – with regards to valuation of the company at $240 per share, this includes valuing the business at $216 per share (at 18x our FY 2016 earnings estimate of $12 per share) plus net cash per share of $24 ($150 billion of net cash less the tax effect on international cash for repatriation, which we estimate to ultimately be 6%, and for simplicity purposes, apply to all cash on balance sheet rather than just the international cash).

Important Disclosure Information

SPECIAL NOTE REGARDING THIS LETTER

THIS LETTER CONTAINS OUR CURRENT VIEWS ON THE VALUE OF APPLE SECURITIES AND ACTION THAT APPLE’S BOARD MAY TAKE TO ENHANCE THE VALUE OF ITS SECURITIES. OUR VIEWS ARE BASED ON OUR ANALYSIS OF PUBLICLY AVAILABLE INFORMATION AND ASSUMPTIONS WE BELIEVE TO BE REASONABLE. THERE CAN BE NO ASSURANCE THAT THE INFORMATION WE CONSIDERED IS ACCURATE OR COMPLETE, NOR CAN THERE BE ANY ASSURANCE THAT OUR ASSUMPTIONS ARE CORRECT. APPLE’S ACTUAL PERFORMANCE AND RESULTS MAY DIFFER MATERIALLY FROM OUR ASSUMPTIONS AND ANALYSIS. WE HAVE NOT SOUGHT, NOR HAVE WE RECEIVED, PERMISSION FROM ANY THIRD-PARTY TO INCLUDE THEIR INFORMATION IN THIS LETTER. ANY SUCH INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. WE DO NOT RECOMMEND OR ADVISE, NOR DO WE INTEND TO RECOMMEND OR ADVISE, ANY PERSON TO PURCHASE OR SELL SECURITIES AND NO ONE SHOULD RELY ON THIS LETTER OR ANY ASPECT OF THIS LETTER TO PURCHASE OR SELL SECURITIES OR CONSIDER PURCHASING OR SELLING SECURITIES. ALTHOUGH WE STATE IN THIS LETTER WHAT WE BELIEVE SHOULD BE THE VALUE OF APPLE’S SECURITIES, THIS LETTER DOES NOT PURPORT TO BE, NOR SHOULD IT BE READ, AS AN EXPRESSION OF ANY OPINION OR PREDICTION AS TO THE PRICE AT WHICH APPLE’S SECURITIES MAY TRADE AT ANY TIME. AS NOTED, THIS LETTER EXPRESSES OUR CURRENT VIEWS ON APPLE. IT ALSO DISCLOSES OUR CURRENT HOLDINGS OF APPLE SECURITIES. OUR VIEWS AND OUR HOLDINGS COULD CHANGE AT ANY TIME. WE MAY SELL ANY OR ALL OF OUR HOLDINGS OR INCREASE OUR HOLDINGS BY PURCHASING ADDITIONAL SECURITIES. WE MAY TAKE ANY OF THESE OR OTHER ACTIONS REGARDING APPLE WITHOUT UPDATING THIS LETTER OR PROVIDING ANY NOTICE WHATSOEVER OF ANY SUCH CHANGES, EXEPT AS NOTED WITH RESPECT TO THE APPLE TENDER OFFER WE ARE ASKING THE APPLE BOARD TO AUTHORIZE. INVESTORS SHOULD MAKE THEIR OWN DECISIONS REGARDING APPLE AND ITS PROSPECTS WITHOUT RELYING ON, OR EVEN CONSIDERING, ANY OF THE INFORMATION CONTAINED IN THIS LETTER.

FORWARD-LOOKING STATEMENTS

Certain statements contained in this letter are forward-looking statements including, but not limited to, statements that are predications of or indicate future events, trends, plans or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties. Forward-looking statements are not guarantees of future performance or activities and are subject to many risks and uncertainties. Due to such risks and uncertainties, actual events or results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Forward-looking statements can be identified by the use of the future tense or other forward-looking words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “should,” “may,” “will,” “objective,” “projection,” “forecast,” “management believes,” “continue,” “strategy,” “position” or the negative of those terms or other variations of them or by comparable terminology.

Important factors that could cause actual results to differ materially from the expectations set forth in this letter include, among other things, the factors identified under the section entitled “Risk Factors” in Apple’s Annual Report on Form 10-K for the year ended September 27, 2014. Such forward-looking statements should therefore be construed in light of such factors, and Icahn is under no obligation, and expressly disclaims any intention or obligation, to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.